Cryptocurrency has transformed from a niche investment into a mainstream asset class, with millions of Americans now holding digital currencies. Yet despite this widespread adoption, the tax implications remain one of the most confusing aspects of crypto ownership. If you’ve bought, sold, or simply held cryptocurrency, understanding your tax obligations isn’t optional—it’s essential for staying compliant with the Internal Revenue Service.

QUICK ANSWER: The IRS treats cryptocurrency as property, meaning every taxable event (selling, trading, or using crypto to purchase goods) triggers capital gains or ordinary income tax. Holding cryptocurrency alone does not create a tax event, but converting one crypto to another, spending crypto on purchases, mining rewards, and selling for fiat currency all require reporting. Failure to report can result in penalties, audits, and interest on unpaid taxes.

AT-A-GLANCE:

| Tax Event | How It’s Taxed | Reporting Form |

|---|---|---|

| Selling crypto for fiat | Capital gains | Schedule D, Form 8949 |

| Trading one crypto for another | Capital gains | Schedule D, Form 8949 |

| Using crypto to buy goods | Capital gains | Schedule D, Form 8949 |

| Mining rewards | Ordinary income | Schedule 1 or Schedule C |

| Staking rewards | Ordinary income | Schedule 1 or Schedule C |

| Airdropped tokens | Ordinary income | Schedule 1 |

| Receiving payment in crypto | Ordinary income | Schedule C or Schedule 1 |

KEY TAKEAWAYS:

- ✅ IRS Classification: Cryptocurrency is property, not currency, per IRS Notice 2014-21 and subsequent guidance

- ✅ Taxable Events: Selling, trading, and spending crypto trigger capital gains; earning crypto through mining, staking, or airdrops triggers ordinary income

- ✅ Holding Period Matters: Assets held less than one year face short-term capital gains rates (up to 37%); held over one year qualify for long-term rates (up to 20%)

- ✅ Reporting Required: The IRS requires reporting on Form 8949 and Schedule D for capital gains; Form 1099 may be required from exchanges in some cases

- ❌ Common Mistake: Many taxpayers believe crypto-to-crypto trades are tax-free—they are not, and the IRS has been explicitly tracking these transactions since 2019

- 💡 Expert Insight: “The biggest mistake I see is people failing to report cross-crypto trades. Every time you exchange one token for another, that’s a taxable disposal with capital gains or losses.” — Tax attorney specializing in digital assets

KEY ENTITIES:

– Government Bodies: Internal Revenue Service (IRS), Financial Crimes Enforcement Network (FinCEN)

– Tax Forms: Form 8949, Schedule D, Schedule 1, Schedule C, Form 1099

– Key Guidance: IRS Notice 2014-21, IRS Revenue Ruling 2019-24, IRS Notice 2023-34

– Tax Rates: Short-term (ordinary income: 10-37%), Long-term (0%, 15%, or 20%)

LAST UPDATED: January 2025

How the IRS Classifies Cryptocurrency

Understanding cryptocurrency taxes begins with recognizing how the IRS classifies digital assets. Since 2014, the IRS has maintained that cryptocurrency is property, not currency. This distinction fundamentally shapes your tax obligations and determines which events trigger reporting requirements.

The IRS first addressed cryptocurrency taxation in Notice 2014-21, released in March 2014. This guidance established that virtual currency is treated as property for federal tax purposes, meaning general tax principles applicable to property transactions apply. This classification means every time you dispose of cryptocurrency—whether through sale, trade, or purchase—you’ve potentially created a taxable event.

The property classification creates several important implications. First, when you acquire cryptocurrency, your cost basis is the amount you paid (or the fair market value if received as income). This cost basis becomes critical when calculating gains or losses upon disposition. Second, the timing of your acquisition matters significantly because holding period determines whether your gains qualify for preferential long-term capital gains rates.

In 2019, the IRS expanded its questioning to explicitly ask about cryptocurrency transactions on tax returns. Schedule 4 of Form 1040 now includes the question: “At any time during 2024, did you receive, sell, exchange, or otherwise dispose of any financial interest in any virtual currency?” This explicit questioning demonstrates the IRS’s focus on cryptocurrency compliance and signals that audit risk for non-reporting has increased substantially.

The IRS has also issued subsequent guidance clarifying specific scenarios. Revenue Ruling 2019-24 addressed hard forks and airdrops, while Notice 2023-34 provided relief for certain decentralized finance transactions. However, many gray areas remain, and the IRS continues to develop guidance as the crypto landscape evolves.

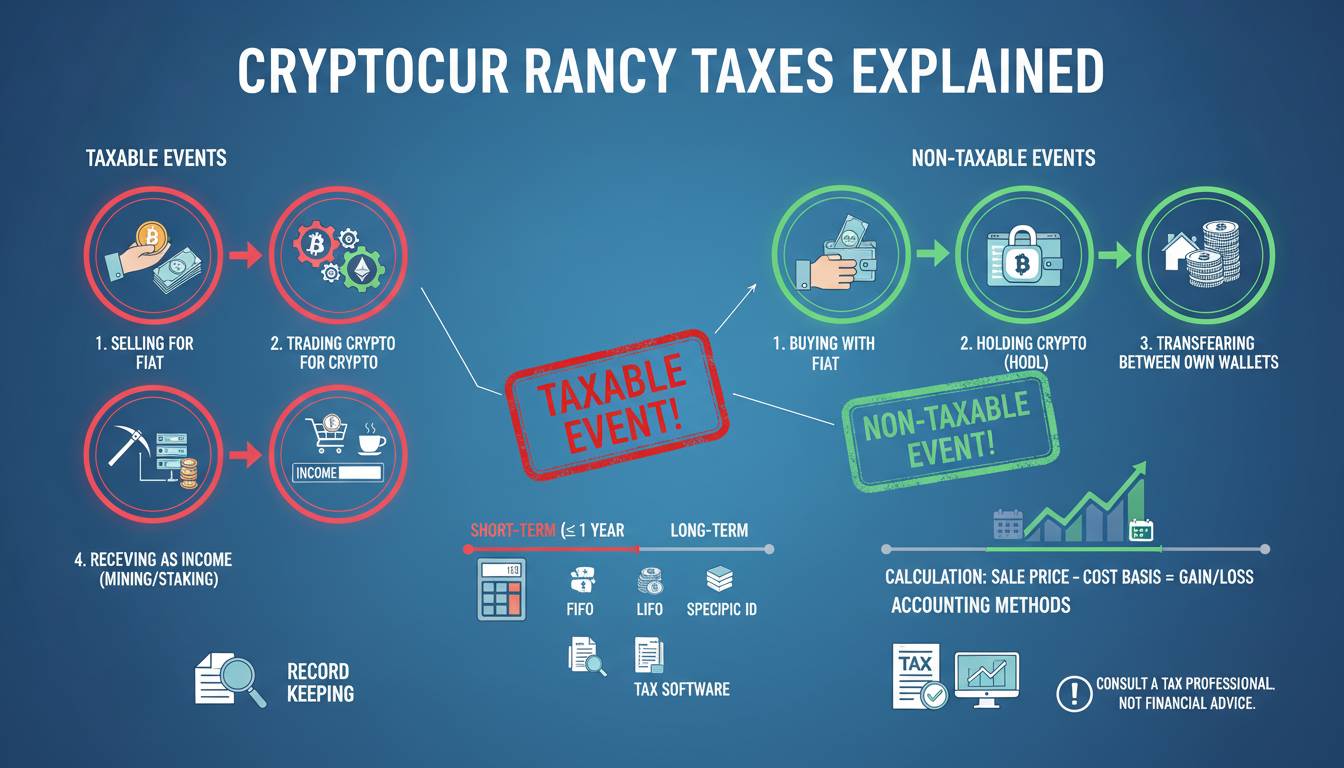

Types of Taxable Events

Not every cryptocurrency transaction creates a tax obligation. Understanding which events trigger reporting—and how they’re taxed—forms the foundation of compliance.

Capital Gains Transactions

Capital gains arise when you dispose of cryptocurrency in exchange for something of value. The most straightforward example is selling cryptocurrency for US dollars. If you purchased Bitcoin at $30,000 and sold it for $50,000, you have a $20,000 capital gain that must be reported.

However, capital gains extend beyond simple sales. Trading one cryptocurrency for another—such as exchanging Ethereum for Solana—constitutes a taxable disposal. You’re selling one asset and acquiring another, even though no fiat currency changed hands. This catch-all provision catches many taxpayers off guard because they believe only “cash-out” events trigger taxes.

Spending cryptocurrency to purchase goods or services also triggers capital gains. If you bought Bitcoin at $10,000 and spent it on a car worth $40,000 when Bitcoin was valued at $40,000, you realized a $30,000 capital gain on that transaction.

The capital gain or loss calculation follows a straightforward formula: proceeds minus cost basis equals gain or loss. Proceeds represent the fair market value of what you received. Cost basis typically includes your purchase price plus any transaction fees that were not separately stated.

Ordinary Income Events

Income events occur when you receive cryptocurrency without disposing of an asset. These transactions create ordinary income equal to the fair market value of the cryptocurrency received, measured in US dollars at the time of receipt.

Mining cryptocurrency creates ordinary income. When you successfully mine a block and receive rewards, that reward is taxable as income at its fair market value on the day received. The same principle applies to staking rewards, which have become increasingly common as proof-of-stake blockchains have grown.

Airdrops—when projects distribute free tokens to holders—also constitute ordinary income. Whether you voluntarily received tokens or they were automatically distributed to wallet addresses, the fair market value of those tokens on the day received must be reported as income.

Forking events create interesting tax scenarios. When a blockchain splits and you receive new tokens from the old chain, that generally creates ordinary income equal to the fair market value of the received tokens. However, this area remains complex, and the specific treatment can depend on whether you had control over the private keys for both chains.

Short-Term vs. Long-Term Capital Gains

The duration of your holding period significantly impacts your tax rate. This distinction provides a meaningful incentive for long-term holding, and understanding it can substantially affect your tax planning.

Short-term capital gains apply when you hold cryptocurrency for one year or less before disposing of it. These gains are taxed at your ordinary income tax rate, which ranges from 10% to 37% depending on your total taxable income. This means short-term gains can face the highest marginal tax rates in the current tax code.

Long-term capital gains apply when you hold cryptocurrency for more than one year before disposal. These gains are taxed at preferential rates: 0%, 15%, or 20% based on your taxable income. For most middle-income taxpayers, the long-term capital gains rate is 15%, which is substantially lower than ordinary income rates that can reach 37%.

Calculating your holding period requires tracking the specific units you disposed of. The IRS allows several methods for identifying which specific cryptocurrency units were sold: specific identification, first-in-first-out (FIFO), or last-in-first-out (LIFO). Each method produces different tax outcomes, and you should choose the approach that best suits your situation while maintaining proper documentation.

Specific identification allows you to identify exactly which units you’re selling when you make the transaction. This method requires documentation at the time of transaction and provides the most flexibility. FIFO—the default method if you don’t specify otherwise—assumes you sell your oldest units first. LIFO assumes you sell your newest units first.

How to Report Cryptocurrency on Your Tax Return

Proper reporting requires understanding which forms to use and where various types of income and gains belong on your tax return. The specific forms depend on the nature of your transactions.

Capital gains and losses from cryptocurrency transactions are reported on Form 8949 (Sales and Other Dispositions of Capital Assets) and carried to Schedule D (Capital Gains and Losses). If your cryptocurrency transactions were through a cryptocurrency exchange that issued Form 1099-DA, you’ll use the information from that form to complete your reporting.

For 2024 and subsequent years, certain cryptocurrency exchanges are required to issue Form 1099-DA (Digital Asset Transactions) for customers who transact at least $10,000 in digital assets. This requirement, part of the Infrastructure Investment and Jobs Act, brings cryptocurrency reporting closer to traditional securities reporting.

Ordinary income from mining, staking, or airdrops is reported on Schedule 1 (Additional Income and Adjustments to Income) as “Other income” if you’re an individual. If you’re engaged in mining as a business, you may need to report income and expenses on Schedule C (Profit or Loss From Business).

Keep in mind that your cryptocurrency tax obligations exist regardless of whether you receive any forms from exchanges. The exchange reporting requirements help the IRS track transactions, but the ultimate responsibility for accurate reporting rests with you. Missing forms don’t excuse non-reporting, and receiving forms doesn’t necessarily mean all your transactions were captured.

The Importance of Record Keeping

Maintaining comprehensive records isn’t just good practice—it’s essential for accurate reporting and protecting yourself if the IRS questions your returns. Without proper documentation, calculating gains and losses becomes impossible, and defending your position becomes extremely difficult.

Every cryptocurrency transaction should be documented with the date, the amount of cryptocurrency involved, the fair market value in US dollars at the time of transaction, the purpose of the transaction, and the counterparty (when applicable). This information allows you to calculate cost basis and determine whether gains or losses occurred.

Your cost basis documentation should include the original purchase price, any transaction fees included in the purchase price, and subsequent improvements or adjustments. For mined cryptocurrency, you need documentation of the fair market value on the day you received the reward.

Many cryptocurrency exchanges provide transaction histories, but these reports have limitations. They may not capture all transactions, particularly those involving transfers between your own wallets or transactions on decentralized exchanges. Your records should supplement rather than replace exchange-generated reports.

Using dedicated cryptocurrency tax software can significantly simplify record keeping. These platforms connect to exchanges via APIs, pulling transaction data and calculating gains and losses according to various cost basis methods. Popular options include CoinTracker, CryptoTaxCalculator, and TokenTax. While these tools help, they’re not infallible, and you should review their calculations for accuracy.

Common Mistakes to Avoid

Understanding common errors helps you sidestep pitfalls that have caught other cryptocurrency taxpayers. These mistakes range from simple oversights to fundamental misunderstandings of tax law.

One of the most prevalent mistakes is failing to report crypto-to-crypto trades. Many taxpayers mistakenly believe these transactions are tax-free because no fiat currency is involved. The IRS explicitly stated in 2019 that exchanging one cryptocurrency for another is a taxable disposition. Each trade requires calculating and reporting capital gains or losses.

Another common error involves losing track of cost basis. When cryptocurrency passes between wallets, exchanges, or is held for years, taxpayers often forget the original purchase price. Without accurate cost basis, calculating gains is impossible, and the IRS will likely treat the entire proceeds as gain.

Ignoring airdrops and forks catches many taxpayers off guard. Even when you receive small amounts of new tokens without specific action, this constitutes taxable income. The income amount equals the fair market value on the day received.

Failing to report transactions on your tax return because you “didn’t receive a 1099” is a dangerous assumption. First, exchange reporting is relatively new and limited. Second, your reporting obligation exists regardless of whether you receive a reporting form. Third, the IRS has increasingly sophisticated tools to track blockchain transactions.

Not consulting a tax professional when your situation is complex can prove costly. If you’re engaged in mining, have significant trading activity, or have transactions spanning numerous platforms, professional guidance helps ensure compliance and may reveal planning opportunities.

Tips for Staying Compliant

Maintaining cryptocurrency tax compliance requires ongoing attention rather than just year-end scramble. Implementing solid practices throughout the year makes tax season far less stressful.

Start by establishing a systematic approach to record keeping. Create a dedicated system for tracking all transactions as they occur rather than attempting to reconstruct them months later. Many investors maintain spreadsheets or use portfolio trackers specifically designed for tax purposes.

Consider the tax implications before executing transactions. If you’re planning to sell a large position, understanding whether you’ll face short-term or long-term rates helps with planning. Sometimes holding an additional few weeks changes your tax treatment substantially.

Review your transaction history regularly, not just at tax time. Monthly or quarterly reviews help catch errors while memories are fresh and documentation is accessible. This practice also helps identify any missing data or gaps that need resolution.

Understand your cost basis method and be consistent. While you can choose different methods for different transactions, maintaining consistency simplifies record keeping and reduces errors. Document your chosen method for each type of transaction.

Plan for tax liability. If you’re actively trading or have significant gains, setting aside funds for tax payment prevents liquidity crunches when payments are due. Remember that capital gains taxes are due in the year of the transaction, not when you file your return.

When to Seek Professional Help

Certain cryptocurrency tax situations warrant professional assistance. Knowing when to engage a tax professional protects both your financial interests and your compliance standing.

If your cryptocurrency activities are substantial—involving significant gains, numerous transactions, or complex structures—professional help is advisable. The cost of expert guidance is typically small relative to the potential savings and risk mitigation.

Engaging a professional makes sense if you’ve received correspondence from the IRS regarding cryptocurrency. Responding to IRS inquiries without professional guidance can easily make a bad situation worse. Tax attorneys with digital asset experience understand the nuances and can communicate effectively with the IRS.

Business activities like mining operations or regular trading generally require professional setup and ongoing guidance. Determining whether activities constitute a business or passive investment affects how income and expenses are reported, with significant tax implications.

Estate planning with cryptocurrency adds another layer of complexity. Properly structuring holdings for estate purposes requires coordinated guidance from tax professionals familiar with both cryptocurrency and estate tax law.

When selecting a professional, look for credentials and experience specific to digital assets. CPAs with cryptocurrency clients, tax attorneys specializing in blockchain, and enrolled agents with relevant experience can all provide valuable assistance. Don’t hesitate to ask about their specific experience with cryptocurrency taxation.

Frequently Asked Questions

Do I have to pay taxes on cryptocurrency if I only held it and never sold?

No, simply holding cryptocurrency does not create a taxable event. Your tax obligation arises only when you dispose of the cryptocurrency through selling, trading, spending, or receiving it as income. The appreciation in value is not taxed until you realize those gains through a taxable disposition.

What happens if I don’t report my cryptocurrency transactions?

Failure to report can result in several consequences, including additional tax assessments with interest, penalties for negligence or substantial understatement, and in extreme cases, IRS audit and criminal investigation. The IRS has increased enforcement focus on cryptocurrency, including matching transaction data from exchanges against reported income.

Can I deduct cryptocurrency losses?

Yes, capital losses from cryptocurrency can offset capital gains from other investments, and up to $3,000 of net capital loss can offset ordinary income each year. Any remaining loss carries forward to future years. However, the wash sale rule—which prevents claiming losses on substantially identical securities—may apply to cryptocurrency in some circumstances.

How do I calculate my cost basis for cryptocurrency?

Your cost basis generally equals what you paid for the cryptocurrency plus any transaction fees. For received cryptocurrency (mining, gifts, airdrops), your basis is the fair market value on the day you received it. When selling, you can use specific identification, FIFO, or LIFO to determine which units are being sold, each producing different tax results.

Do I need to report small transactions or small amounts of cryptocurrency?

Yes, there’s no minimum threshold for reporting. Every taxable event must be reported regardless of the amount. Even receiving small airdropped tokens creates taxable income that must be reported. The IRS requires reporting on all transactions, and the requirement applies equally to small and large amounts.

Are there ways to reduce my cryptocurrency tax liability?

Several strategies can help minimize tax liability. Holding cryptocurrency for more than one year before selling converts short-term gains to long-term gains taxed at lower rates. Tax-loss harvesting involves selling losing positions to offset gains. Strategic timing of transactions can also help. However, avoid artificial tax avoidance schemes that the IRS might challenge. Always maintain proper documentation and consider consulting a tax professional for personalized guidance.

Conclusion

Cryptocurrency taxation presents genuine complexity, but understanding the fundamentals helps you navigate compliance confidently. Remember that the IRS treats cryptocurrency as property, meaning virtually every disposition triggers potential tax consequences. The key to staying compliant lies in understanding which events create tax obligations, maintaining accurate records, and reporting properly on your tax return.

Start by establishing good record-keeping practices now. Track every transaction with dates, values, and purposes. Use cryptocurrency tax software to help organize your data and calculate gains. Review your situation regularly to catch problems early.

Most importantly, don’t ignore your obligations hoping the issue will disappear. The IRS is actively enforcing cryptocurrency tax compliance, and the penalties for non-compliance can be severe. If your situation is complex, professional guidance from a tax practitioner with cryptocurrency experience provides both protection and peace of mind.

Approach cryptocurrency taxation proactively rather than reactively. By understanding your obligations throughout the year—not just at tax time—you’ll be better positioned to comply with the law, minimize your tax liability legally, and avoid the stress of IRS correspondence. Cryptocurrency offers genuine financial opportunities; understanding the tax implications ensures you can enjoy those benefits without unexpected complications.

{kind=link}

Leave a comment